On September 11, 2014, 8 traders were indicted on duping almost $300 million out of mom and pop investors [1]. How do you avoid this trickery and avoid buying stocks for companies that are “shells”?

The answer is simple- look at the company’s market capitalisation. These fraudster’s companies usually have a very small amount of market capitalization if any reported and shown, such as less than two million dollars. Any major fraud involving the stock price of a multi billion dollar company is rare and will get news coverage equivalent to what Enron or MCI Worldcom received in the 90’s and early 2000’s. My rule of thumb is to never invest in companies with less than 300 million in market capitalisation. Looking at the integrity of the company’s website is not a sure way of knowing if you are dealing with a legitimate company. After market capitalisation, you should avoid buying shares ‘Over The Market’ – instead stick with companies listed on the Dow Jones or Nasdaq.

One of the websites they channelled their spam through was called ‘pennypic.com’, and of course now the website is offline. In order to research what type of stocks these fraudsters had I used the WayBackMachine on web.archive.org.

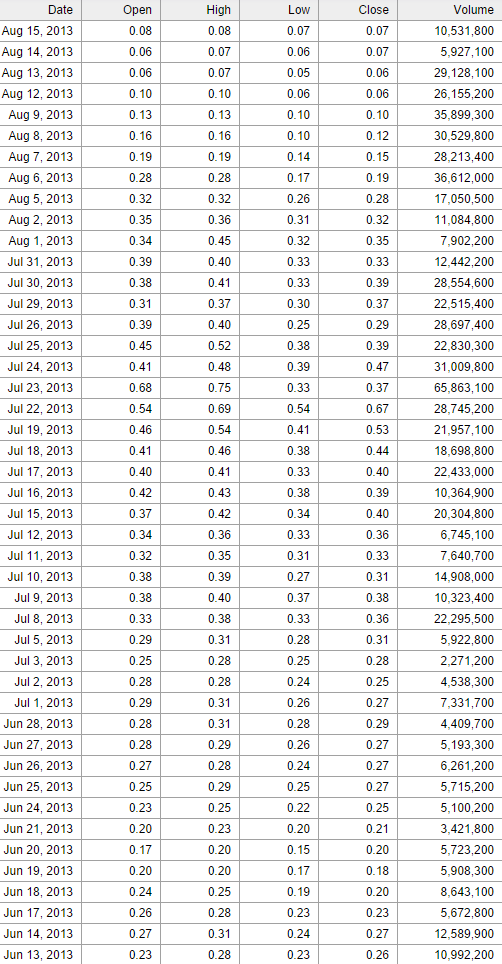

Take a look at XUII, it was the symbol blaring on their unbecoming website as their “Monster Pick”, it now trades at $0.0003 per share on the over the counter market (a.k.a. bankrupt) – take a look at it’s price history starting on June 13th when they were advertised.

Scammers inflate the price to draw more people in along with sending spam, then they dump the stock.

As you can see the price was 23 cents on June 13th, and inflated to almost 68 cents when the scammers started selling – pushing the stock down to 6 cents in just two months.

[1] Rosenburg, Rebecca. “8 Traders Indicted in $300M Pump and Dump.” New York Post. New York Post, 11 Sept. 2014. Web. 11 Sept. 2014.